Market Review - Feb/Mar 2021

Housing index reflects new life

Housing index reflects new life

The FNB House Price Index for the third quarter of 2020 recorded a 12-month average growth of 0.7% y/y as at September 2020. This is the first time in nearly three years that the index portrays growth. This rebound in house prices affirms FNB’s earlier view that the price deceleration was reaching a plateau. The national weighted average house price as at September 2020 was N$ 1 233 106.

The increase in house prices has been partly fuelled by the completion of new developments in the central area. Moreover, the persistently strong demand for residential land in smaller towns might also have contributed to the rebound. This is particularly true for the southern and northern regions where land appears to be relatively affordable.

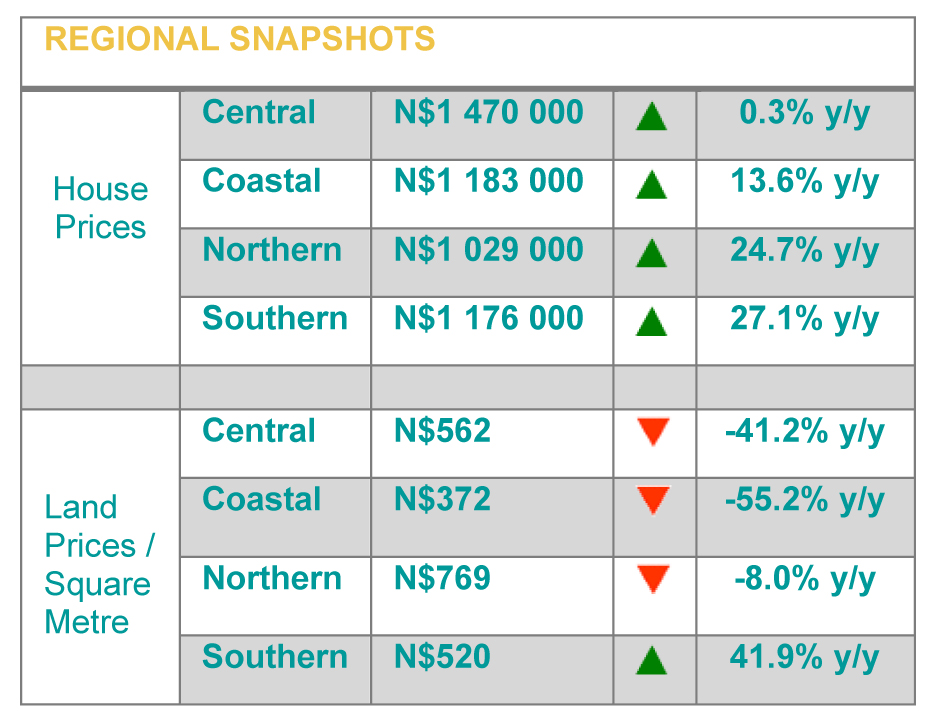

Land prices in the southern region grew by 41.9% y/y compared to a contraction of 27.3% y/y recorded a year ago. The central, coastal and southern regions, on the other hand, recorded contractions in land prices of 41.2%, 55.2% and 8.0% y/y respectively over the reviewed period. This is not surprising, given the overwhelming dominance of first-time buyers in the market. Overall demand for housing remains highly concentrated in the small and medium market segments with growth recorded as 11.6% and 33.4% y/y, respectively.

Central residential property prices grew by 10.8% y/y compared to a contraction of 5.2% y/y recorded over the same period of 2019. On average, a house in the central region is now priced at N$ 1 470 000. When looking at major towns, the 12-month average price for a house in Windhoek came in at N$ 1 089 000, having contracted by 8.6% q/q and 4.6% y/y. Similarly, Okahandja and Gobabis recorded annual contractions in house prices of 3.3% and 11.9% y/y to N$ 765 000 and N$ 665 000, respectively.

In the central region, year-on-year growth was recorded at 9.2%, compared to a growth of 2.5% y/y recorded a year ago. This reflects improved trading activity across all the housing segments. However, the small and medium housing segments remain the core market for this region from an affordability point of view.

House prices in the coastal region remain high, averaging N$ 1 183 000 at the end of September 2020. This reflects a price growth of 13.6% y/y compared to a contraction of 5.4% y/y recorded over the same period of 2019. The small housing segment has been and continues to be a core market for the region due to the relative dominance of industrial jobs. The medium to higher-end market segments appear to be highly dominated by investment properties. In essence, the 12-month average price for a house in Swakopmund, Walvis Bay and Henties Bay is recorded at N$ 727 000, N$ 721 000 and N$ 772 000, respectively.

At the coast, the growth was 10.7% y/y. This is a marked improvement when compared to a contraction of -29.4% recorded over the corresponding period of 2019 and points to completion of new developments within the small housing segment.

Northern house prices remain buoyant, recording a four-year record growth of 24.7% y/y. The 12-month average house price in the northern region is now calculated at N$ 1 029 000 from N$ 825 000 recorded in the same period of 2019. This is reflective of an improvement in the delivery of residential land especially in Oshikuku, Outapi, Katima Mulilo and Rundu. In effect, house prices in these towns respectively grew by 35.1%, 11.9%, 66.1% and 4.55 y/y.

The northern volume index grew by 24.6% y/y from 28.8% y/y recorded in the same period of 2019. The housing demand will likely increase further in anticipation of the government’s rollout of the “Upgrading of Informal Settlements” plan to the rest of the regions.

The southern region recorded a significant growth in house prices of 27.1% y/y from 15.3% y/y recorded a year ago. This points to ongoing residential development projects in Mariental. The 12-month average house price in the southern region is now calculated at N$ 1 176 000 from N$ 925 000 recorded over the same period of 2019. However, the southern region only makes up about 3 percent of overall national transactional volumes, hence the volatility in prices over time.

As the availability of affordable houses continues to take a toll on the housing market, accessibility and affordability of land becomes an important force towards market stabilization. Meanwhile, the growth in land delivery has been trending downward since the beginning of 2020, reaching 21.3% y/y at the end of September 2020. This suggests the need for renewed political momentum as far as the acceleration of land delivery is concerned.

The housing market has been much more resilient than many analysts had predicted at the outset of the pandemic. FNB remains optimistic about further growth in house prices on the back of the persistent housing backlog. The change in political leadership at the City of Windhoek may renew the momentum of accessible and affordable land delivery, particularly for low and ultra-low-income households. Market dynamics will likely continue to be shaped by the desire for more residential outdoor space and by relocation to smaller towns, as the culture of remote working gains prominence.

Frans Uusiku

Marketing Research Manager

For more information, please call: 061 – 299 2222 or visit www.fnbnambia.com.na